Consumer Compliance Outlook Publishes First Issue of 2020

With everything going on these days, some may have missed the recent publication by the Philadelphia Federal Reserve’s helpful Consumer Compliance Outlook. The first article was a rather helpful summary of most common compliance issues the Fed found over multiple years of exams. These fit into the following categories:

- Regulation B – requiring spousal signatures

- Flood insurance rule – purchase and force-placement requirements

- Regulation Z – understating finance charges

- Fair Credit Reporting Act – adverse action notice requirements

Here’s a summary of these findings and some of the tips provided by the article.

Regulation B

The Equal Credit Opportunity Act and its implementing Regulation B, in part, prohibit creditors from discriminating in a credit transaction on any “prohibited basis” which includes but is not limited to race, religion, age, and ethnicity, sex and marital status. One common violation the Fed observed related to section 1002.7(d) of the rule which states that a credit union generally cannot require the signature of a spouse on a loan application when the spouse is not a joint applicant for credit and the applicant qualifies individually.

There are some specific exceptions to the general rule against requiring the spouse’s signature when the application is not joint. For example, one relates to situations where the spouse’s signature is needed under state law in order to provide the credit union with access to collateral used to secure the property. For example, state law may require the spouse’s signature to create a lien in certain property. The full list of exceptions may be worth reviewing.

The Fed found that often, there were strong controls in their regulated institutions for consumer loans in this area, but weaker controls in commercial or agricultural loans. The Fed also found some misunderstandings of when a signature may be needed to have rights to collateral under state law. Some exams showed creditors seeking the spouse’s signature out of an “abundance of caution,” not because that was necessary to have a lien in property relied on or used as collateral in the credit decision.

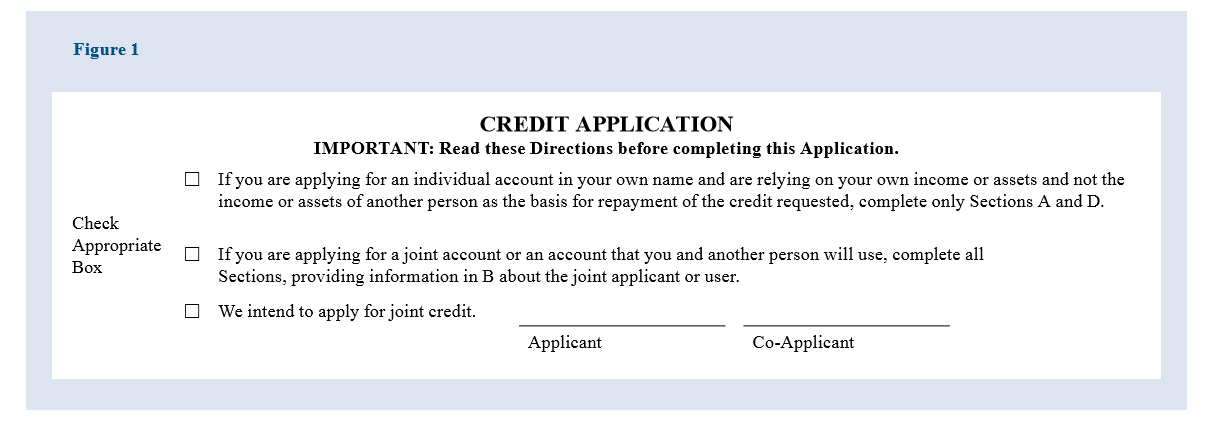

Additionally, if there is a joint application, the rule’s commentary indicates there needs to be evidence of intent to be joint applicants at the time of application. Other common mistakes related to how to demonstrate intent to apply for joint credit. One of the article’s compliance risk management suggestions was an example of how to document that spouses intended to apply for credit jointly:

Flood Insurance

Certain loans require the purchase of flood insurance under section 760.3. Apparently the Fed found sometimes there were not procedures in place at some institutions to determine if flood insurance was required, or ensure the required amount of coverage was in place. Some of these violations seem to have occurred in the context of third-party vendor relationships. The article suggests developing checklists and having a secondary review as possible tools for preventing this kind of violation.

The rule also has requirements to force place flood insurance in some situations, set forth in section 760.7. Common violations in this area included: failure to flag that a property that was previously not in a flood zone was remapped and then act on that in a timely manner; not verifying a property that lapsed was renewed for the required amount of coverage; and not sending the required notice after finding coverage was lapsed or not force-placing insurance 45 days after sending a notice. To address these issues, the article suggested using a vendor to monitor flood map changes for the life of loans, having monitoring and audit programs, a system to provide notice when policy renewal dates are approaching and appropriate training for staff.

Regulation Z

Section 1026.4 of Regulation Z determines which costs are finance charges for the purposes of disclosing the annual percentage rate to borrowers. This can be particularly complicated for residential mortgages given that some fees may or may not be excluded depending on the particular terms of the transaction. One common violation the Fed noted was understating the finance charges for closed-end residential mortgages, citing tolerances applicable prior to the effective date of TRID. Another common violation involved loan software platforms that allowed the loan processor to bypass the proper finance charge designation when setting up required disclosures. The article suggested policies and procedures that provide a detailed representation of all of the lender’s applicable loan fees and when they may be deemed prepaid finance charges. The article also suggested heighted oversight when installing new automated loan software.

FCRA

Finally, the FCRA requires notice whenever a credit union takes an adverse action against a consumer based in whole or in part in information in a consumer report. The FCRA defines consumer report in a much broader way than just credit reports, such as ChexSystems reports. But if a credit score was relied on, the FCRA requires disclosure of the score, the name of the consumer reporting agency that created the score and how to obtain a report from that agency. What was the common violation here?

The Fed found that often, FCRA adverse action notices were missing required information like the credit score disclosures. The article again suggested oversight of software, training, policies and procedures, checklists, audits, and monitoring as key ways to mitigate the risk of violations.

Overall, this article provided a helpful summary of these key rules and some practical compliance considerations in these areas. Compliance officers tasked with reviewing these topics may find the full article helpful.

About the Author

Brandy Bruyere, NCCO, Vice President of Regulatory Compliance/Senior Counsel, NAFCU

Brandy Bruyere, NCCO was named vice president of regulatory compliance in February 2017. In her role, Bruyere oversees NAFCU's regulatory compliance team who help credit unions with a variety of compliance issues.

Brandy Bruyere, NCCO was named vice president of regulatory compliance in February 2017. In her role, Bruyere oversees NAFCU's regulatory compliance team who help credit unions with a variety of compliance issues.