Federal Regulators Provide Temporary Relief for Credit Unions Approaching $10 Billion

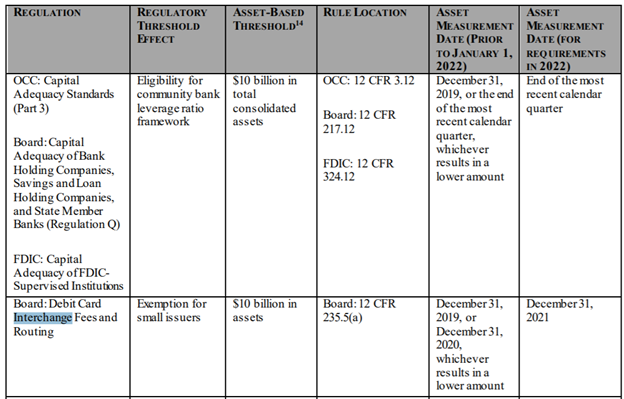

On November 20, 2020, the Federal Reserve along with the FDIC and OCC published an interim final rule to mitigate the costs to banks of crossing asset-based regulatory thresholds sooner than expected. Just in time for Thanksgiving, the rule permits banks under $10 billion in total assets as of December 31, 2019 (community banking organizations) to use asset data as of December 31, 2019, in order to determine the applicability of various regulatory asset thresholds during calendar years 2020 and 2021. One of the significant thresholds covered under the rule is the trigger for debit interchange caps, which were instituted by the Durbin Amendment as part of the Dodd-Frank Wall Street Reform and Consumer Protection Act. The Durbin Amendment modified the Electronic Fund Transfer Act (EFTA) to restrict the routing and pricing of electronic debit transactions by card issuers, and the Federal Reserve has implemented these statutory provisions in Regulation II (12 CFR Part 235).

From an advocacy standpoint, NAFCU opposes interchange price caps, which have had the effect of depressing credit union fee income while transferring wealth to retailers. One recent study of interchange doubts whether this transfer corresponded with any meaningful benefit to consumers, but does note evidence of higher retailer margins.

For most credit unions, the transition to interchange compliance can be managed adequately with planning. But some have grown faster than expected in 2020 and are eager to take advantage of any mechanism to avoid an unexpected hit to their bottom lines. The interim final rule explains that a community banking organization that was below an asset threshold covered by the rule (e.g., the $10 billion threshold applicable to small issuers under § 235.5) as of December 31, 2019, generally will be deemed to remain below that threshold through the end of 2021. The second to last column in the chart below illustrates how this framework effectively delays recognition of asset growth and postpones compliance. The last column illustrates that the relief is temporary and the default asset measurement approach will resume after 2021.

Credit unions nearing the $10 billion threshold may be wondering whether this relief also applies to them given that the preamble and press release issued in conjunction with the rule focus on the relief’s applicability to community banking organizations, a term that appears frequently throughout the notice. A plain reading of the amendments suggests that the interchange amendments do afford relief to credit unions. The new language added to Part 235 does not make use of the “community banking organization” term and instead refer to issuers, consistent with the existing regulatory terminology found in Part 235. The term issuers is defined 235.2(k) as “any person that authorizes the use of a debit card to perform an electronic debit transaction. The definition is broad enough to encompass banks and credit unions.” The commentary to this definition refers to “banks and other entities.”

The language of the amendment in the interim rule reads as follows:

§235.5 Exemptions. * * * * *

(a) * * *

(4)(i) Temporary Relief for 2020 and 2021. Except as provided in paragraph (a)(4)(ii) of this section, for purposes of determining eligibility for the exemption for small issuers described in paragraph (a)(1) of this section, issuer asset size that is calculated as of the end of the calendar year 2020 shall be determined based on the lesser of:

(A) The assets of the issuer, together with its affiliates, as of the end of the calendar year 2019; and

(B) The assets of the issuer, together with its affiliates, as of the end of the calendar year 2020.

(ii) The relief provided under this paragraph (a)(4) does not apply to an issuer if the Board determines that permitting the issuer to determine its assets in accordance with that paragraph would not be commensurate with the asset profile of the issuer. When making this determination, the Board will consider all relevant factors, including the extent of asset growth of the issuer since December 31, 2019; the causes of such growth, including whether growth occurred as a result of mergers or acquisitions; whether such growth is likely to be temporary or permanent; whether the issuer has become involved in any additional activities since December 31, 2019; the asset size of any parent companies; and the type of assets held by the issuer. In making a determination pursuant to this paragraph (a)(4)(ii), the Board will apply notice and response procedures in the same manner and to the same extent as the notice and response procedures in 12 CFR 263.202

In general, small issuers (i.e., those under $10 billion in assets) are exempt from interchange price caps found in section 235.3, as well as the provisions in sections 235.4 and 235.6.

Credit unions that are hopeful of leveraging the new relief should also note the catchall provision in new section 235.5(a)(4)(ii). This paragraph provides the Federal Reserve with discretion to determine whether an issuer is ineligible for the exemption. The Board might consider, for example, whether asset growth was truly the result of a flight to safety caused by the pandemic or connected with a deliberate business strategy of growing very quickly. Based on commentary found in the preamble, relief is generally intended to mitigate unexpected asset growth connected with the temporary exigencies of the pandemic.