NCUA Approves CECL Policy Statement; HMDA Annual LAR Deadline

During the National Credit Union Administration (NCUA) Board's February 2020 meeting, the NCUA Board approved the final Interagency Policy Statement on Allowances for Credit Losses (Policy Statement). NCUA, together with the three other federal banking agencies, issued the Policy Statement in response to changes to U.S. generally accepted accounting principles (GAAP) due to the adoption of the current expected credit losses (CECL) methodology.

While NAFCU has been successful in lobbying the Financial Accounting Standards Board (FASB) to delay CECL (credit unions do not need to comply with CECL until January 2023) and continues to ask for reconsideration of the standard, credit unions should not presume that CECL is going away. Regardless of how far along a credit union may be in terms of implementing the new standard, the Policy Statement is an essential document that will help credit unions understand the NCUA's expectations related to CECL and allowances for credit losses. Because of the resources that are required to implement CECL (e.g., more data, additional staff, etc.) and the time it will take to implement CECL, a frequently asked questions document prepared by NAFCU has noted that many sources have advised credit unions to have CECL in place at least a year before the effective date to permit running CECL and the incurred loss model at the same time. The rationale for this proposed dual tracking includes being able to refine CECL processes before they are mandatory. Moreover, NCUA has included CECL on its list of 2020 supervisory priorities, and examiners will discuss CECL implementation plans with credit union management during examinations.

CECL Background

Before examining the Policy Statement, it may be helpful to discuss CECL at a very high level and how it may impact a credit union's allowances for credit losses. The CECL methodology was developed by the FASB as a response to the financial crisis that began in the 2000s. Before CECL, GAAP required the incurred loss methodology in which credit losses were not recognized until it became probable or likely that a loss was incurred. Some people were distressed that credit losses that were expected but did not satisfy the probable threshold could not be recognized under the incurred loss methodology. The FASB and proponents of CECL have argued that the standard is necessary to correct for delayed recognition of credit losses under the incurred loss methodology, which might lead to an overstatement of assets.

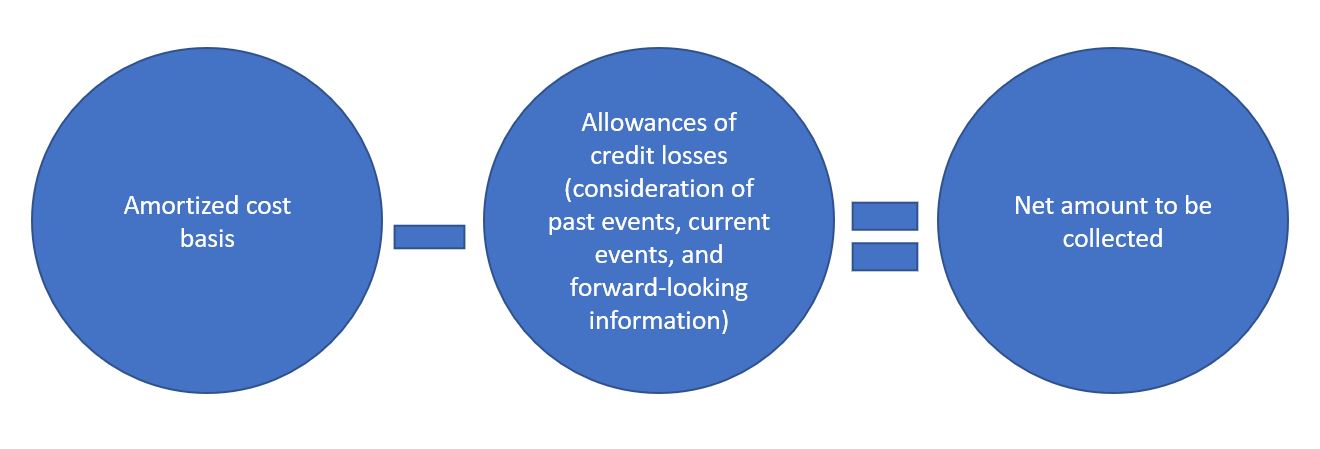

In the most basic terms, the CECL standard requires three components in the measurement of expected credit losses. The first component is information about past events: This encompasses a credit union's historical loss data. The second component is what effect current conditions may have on expected credit losses. The final component, and maybe the most difficult to deal with on an operational level, are reasonable and supportable forecasts that affect future collectability. The components of CECL evidence an emphasis on a forward-looking process in measuring expected credit losses as opposed to waiting for a loss to be probable or likely.

CECL affects a credit union's allowances for credit losses because the measurement of expected credit losses influences the net amount of how much the credit union believes it will collect. Here is a simplified formula derived from the Policy Statement that demonstrates how this works:

The Policy Statement

The Policy Statement does a couple of things. First, it is effective when each institution adopts CECL. At that point, other policy statements - like NCUA's Interpretive Ruling and Policy Statement 02-3 that examines allowances for loan and lease losses under the incurred loss methodology - will no longer be effective. The agencies clarify that they intend to formally rescind these other policy statements once all institutions are subject to CECL.

Second, the agencies note in the Policy Statement that credit unions have a good deal of discretion and flexibility in implementing CECL. In other words, there is no one-size-fits-all prescription. CECL implementation can be tailored to a credit union's size, complexity, structure, strategies, and risk tolerances.

Third, it provides guidance about

- measuring expected credit losses under CECL;

- designing, documenting, and validating expected credit loss estimation processes;

- maintaining an appropriate level of allowances for credit losses

- the separate responsibilities of the board of directors and management; and

- what examiners may look for when reviewing allowances for credit losses.

For the purpose of this blog, it would be impossible to go into significant detail about the practical application of this guidance. Much of it is technical in scope and requires more than just a passing familiarity with accounting concepts. That said, the discussion in the Policy Statement about historical loss considerations may provide compliance professionals with an illustrative example of what kind of information is included and what may be helpful. At the very least, it should make it somewhat easier for credit unions to communicate their CECL implementation progress in a way that is satisfactory to examiners.

The Policy Statement emphasizes that historical credit loss information, regardless of whether it is internal or external information or some combination of the two, can provide a focal point for a credit union's assessment of expected credit losses. The Policy Statement cautions credit unions to consider whether adjustments to historical loss information need to be made to the extent that current conditions and reasonable and supportable forecasts may differ from the historical loss timeline. For example, if the credit union's historical credit loss data only goes back to 2012 and only captures a recovering economy, does the historical credit loss data need to be adjusted if current conditions are different? Here, we see an example of how current conditions and reasonable and supportable forecasts may shape a credit union's assessment of its historical credit loss information.

The Policy Statement notes that a credit union's policies and procedures relating to the allowances for credit losses should address how the credit union determines an appropriate historical period to use in light of differences in assets being analyzed, current conditions, and reasonable and supportable forecasts. As the Policy Statement suggests, the emphasis on a forward-looking process needs to be captured in the relevant policies and procedures.

The Policy Statement provides that examiners may evaluate a credit union's policies and procedures to see whether management's consideration of historical loss information, current conditions, and reasonable supportable forecasts is appropriate under the circumstances. In short, the Policy Statement provides credit union compliance professionals with a high-level overview of some of the compliance concerns that may arise during the implementation of CECL.

HMDA Submissions and March 1st Falling on a Weekend

Because March 1st falls on a Sunday this year, section 1003.5(a)(1)(iii) of Regulation C permits submission of a HMDA annual loan/application register (LAR) on Monday, March 2nd. Under Regulation C, the submission of a LAR on Monday - at least this year - would be considered timely.