This is Not a Drill: Small Window to Enroll in SSA’s New Electronic Consent Based Social Security Number Verification Service

Written by Mahlet Makonnen, Regulatory Affairs Counsel

We have received questions from members on how the Social Security Administration’s (SSA) recent notice on enrollment for an electronic Consent Based Social Security Number (SSN) Verification (eCBSV) service affects credit unions. With the initial enrollment deadline just around the corner on July 31, 2019 at 6 PM Eastern, financial institutions must decide quickly whether to sign up for this new database or potentially wait up to two years for the next opportunity to enroll. We are here to explain the background and more details on the timeline of SSA’s notice as well as what to expect in terms of cost.

Why a New eCBSV?

Signed into law on May 24, 2018, Section 215 of the Economic Growth, Regulatory Relief, and Consumer Protection Act requires the SSA to modify or develop a database for accepting and comparing fraud protection data (defined to include a combination of an individual’s name – the first name and any family forename or surname –SSN, and date of birth) provided electronically by a permitted entity. The bill also requires the new database to accept the electronic consent of an individual to allow a financial institution to verify his or her name, date of birth, and SSN using the SSA’s eCBSV. The Act defines “permitted entity” to mean a financial institution or service provider, subsidiary, affiliate, agent, subcontractor, or assignee of a financial institution. 42 U.S.C. 405b(b)(4).

In response to the Act, the SSA published a notice in the Federal Register in June 2019 outlining the SSA’s initial enrollment period for the new eCBSV service. The SSA published this notice without an opportunity for a comment from the public. NAFCU has been engaged with the agency since the Act was signed into law and the SSA began looking at how to implement the requirements in Section 215.

What is the Initial Enrollment Deadline?

The SSA is expecting to implement the initial rollout of its eCBSV in June 2020 to a limited number of permitted entities who submit a valid application by the close of the above deadline. Then, the SSA is planning an expanded rollout to all permitted entities that applied for the initial rollout but were not selected within the six months following the initial rollout. In the notice, the SSA provides “permitted entities” with a narrow, two-week enrollment period. The enrollment period to apply for access to eCBSV began July 17, 2019, at 6 a.m. EST, and closes on July 31, 2019, at 6 p.m. Eastern.

Notably, financial institutions that do not submit a valid application before the close of the July 31, 2019 deadline:

· Will not be eligible to apply for the expanded rollout in late 2020; and

· Must wait until the next open enrollment period, which could be up to two years later.

How Much Does Participation in the eCBSV Cost?

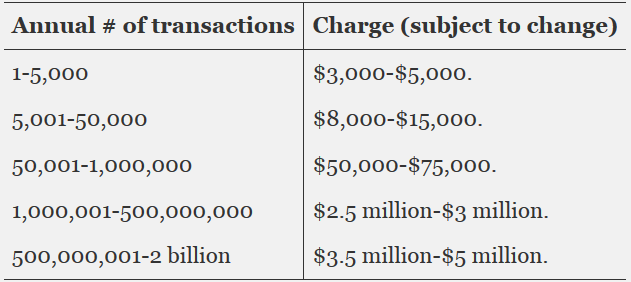

The long-term costs associated with the eCBSV are uncertain given that this is the first enrollment opportunity for financial institutions; however, there is a statutory requirement for the program startup costs. The Act requires the SSA to collect 50 percent of the program startup costs prior to developing the eCBSV system. Accordingly, once a permitted entity is selected and notified by the SSA, that entity will receive a bill to pay their prorated portion of 50 percent of the estimated program startup costs within two weeks of selection. The SSA notes that these funds will be credited to future transactions. A chart from the SSA’s notice containing a breakdown of expected contribution of the 50 percent program startup costs is replicated below:

It is important to recognize that the prorated portion of the cost of the program is subject to change because it depends on the number of permitted entities selected, the estimated annual transaction volumes, and the associated costs. As such, selected permitted entities will be notified of this cost once enrollment ends and all of the dependent factors are finalized. Moreover, every permitted entity selected will be required to pay an initial administrative fee of $3,693 and an annual tier-based transaction charge based on their estimated annual volume.

For those permitted entities that apply during the expanded rollout, fees will include an administrative fee and an annual tier-based transaction charge adjusted based on the new enrollment period. The remaining program start-up costs will be collected from all users during the first year of eCBSV.

So, ultimately costs for your credit union to participate could include:

· A prorated share of 50 percent of the estimated program startup costs;

· An initial administrative fee of $3,693; and

· An annual tier-based transaction charge based on a credit union’s estimated annual volume.

What Are the Next Steps?

Credit unions must quickly perform a cost benefit analysis to determine whether to enroll during the initial enrolment period. Keep in mind that those permitted entities who fail to enroll by the July 31 deadline have to wait for the next enrollment period, which could be as long as two years away. Consequently, a credit union that misses this enrollment period could potentially be left in the dark about what the new the eCBSV system looks like. If, after considering all of these factors, your credit union wishes to enroll, please review the SSA’s notice, complete the enrollment form, and submit the form by next week’s deadline.

NAFCU continues to engage the SSA on this issue and has urged the SSA to work with the NCUA to ensure that implementation of this new fraud protection database does not create additional regulatory burdens for credit unions. NAFCU plans to work with the SSA to address credit union concerns related to the creation of eCBSV and will update you as we continue to monitor the implementation of this new database.