STOP! In the Name of Regret: Handling Stop Payment Requests for Recurring Debits

We’ve all been there… January first rolls around and our brains jump into overdrive thinking about all the things we are going to accomplish in the coming year. Whether it’s joining a gym to get back in shape, taking that pilates class we’ve been eyeing for months or registering for a meal delivery service in our never-ending quest to eat healthier, we have all signed up for something that felt like a great idea in the post-New Year’s haze of optimism. But, by March, reality sets in, old habits take over and we know there just aren’t enough hours in the day to do all the things we want.

Your members are no different. Complaints about how the yoga studio down the street just keeps billing every week no matter how many times you tell them to cancel are not that uncommon this time of year. It is important for credit unions fielding these types of complaints to be aware of their responsibilities when receiving stop payment requests for recurring debits from a member’s account.

Recurring debits, or preauthorized transfers as they are known under Regulation E, are those transfers that happen on a regular basis to a member’s deposit account. They can occur weekly, bi-weekly, monthly or in any other interval as long as the interval is the same each time. They can also vary in amount from transfer to transfer. The key is that they happen regularly without the member having to do anything each time. If your credit union receives a request to stop a recurring debit, there are specific rules that must be followed.

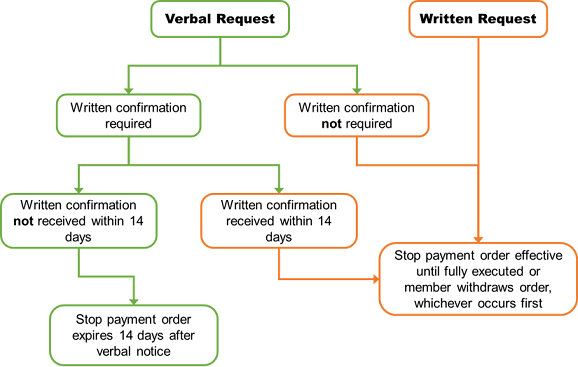

First things first: verbal requests are valid too. Under both section 1005.10(c)(2) of Regulation E and Article Three of the NACHA Operating Rules, verbal and written requests to stop payment trigger a credit union’s responsibilities. However, there are differences in how long a request is valid based on whether it was a verbal or written request.

If a credit union requires a written confirmation, then verbal requests are effective for fourteen days. The rules require credit unions to inform members that a written confirmation is required and where to send it when it receives a verbal request. If the written confirmation is not received within fourteen days, the verbal stop payment order expires.

Written stop payment orders, written confirmations of verbal orders and verbal orders where no written confirmation is required are effective until they have been fully executed or are withdrawn, whichever occurs first. Recurring debits are fully executed when all entries in the series have been stopped. Credit unions may not allow any transfers subject to a stop payment order to post to the member’s account. For recurring debits, credit unions may require members to confirm in writing they have properly revoked authorization with the merchant.

This chart illustrates the time frames applicable to both verbal and written stop payment requests:

Then some other important things: requests must be received in time for a credit union to act on it. Under Article Three of the NACHA Operating Rules, all requests provided by the member at least three banking days before the scheduled date of the entry must be honored. A “banking day” is any day, or partial day, the credit union is open to the public for “carrying on substantially all of its banking functions.”

Under section 1005.10(c)(1) of Regulation E, all requests provided by the consumer at least three business days before the scheduled date of the transfer must be honored. A “business day” is any day the credit union is open to the public for “carrying on substantially all business functions.” The commentary explains both public functions and back-office operations must be open for a credit union to be carrying on substantially all business functions.

In most cases, a credit union’s banking days will be the same as its business days; but it is important to understand that this may not always be true and to know whether this is the case for your credit union. Properly executing stop payment requests is not only a requirement under the rules but it can also help prevent unauthorized transactions from posting to a member’s account which may require the credit union to complete the error resolution process. For more on stop payment orders, check out this Compliance Monitor article (member-only).