CDFI Refresher and Helpful Resources

The Federal Reserve Board published the first 2022 issue of its Consumer Compliance Outlook, which includes a feature article on Community Development Financial Institutions (CDFIs) and their impacts on the financial system. The article starts by explaining that CDFIs are mission-focused financial institutions, specifically providing services to “underserved communities, including LMI [low to moderate income] consumers, communities of color, women, or minority groups who can experience challenges accessing credit” while also helping to “grow local economies, provide affordable housing, and support small minority-owned businesses.” The Department of Treasury regularly reviews the activities of CDFIs to ensure they are still working toward the mission of helping their designated communities. According to the Treasury, CDFIs can be found in every state.

The article goes on to describe how CDFIs operate and the importance of access to funding. Generally, CDFI’s attempt to offer services and products at low or no costs to the target community. For example, a CDFI mortgage lender may be more willing to make smaller mortgage loans that do not generate enough interest and fee income to support the cost of making the loans. In this case, the CDFI would make the loan in order to expand lending and financial opportunities in the community, and rely on donation, grants, and other funds to cover the costs of offering these loans. CDFI credit unions also rely on member (and to a limited extent, nonmember) deposits to support their operations. Due to the mission and requirements of certification for CDFIs, these organization play a key role in expanding financial inclusion to markets that are in need, especially during times of crisis, such as during the pandemic. CDFIs must be creative and strategic in leveraging funds from a variety of sources in order to provide for communities in need.

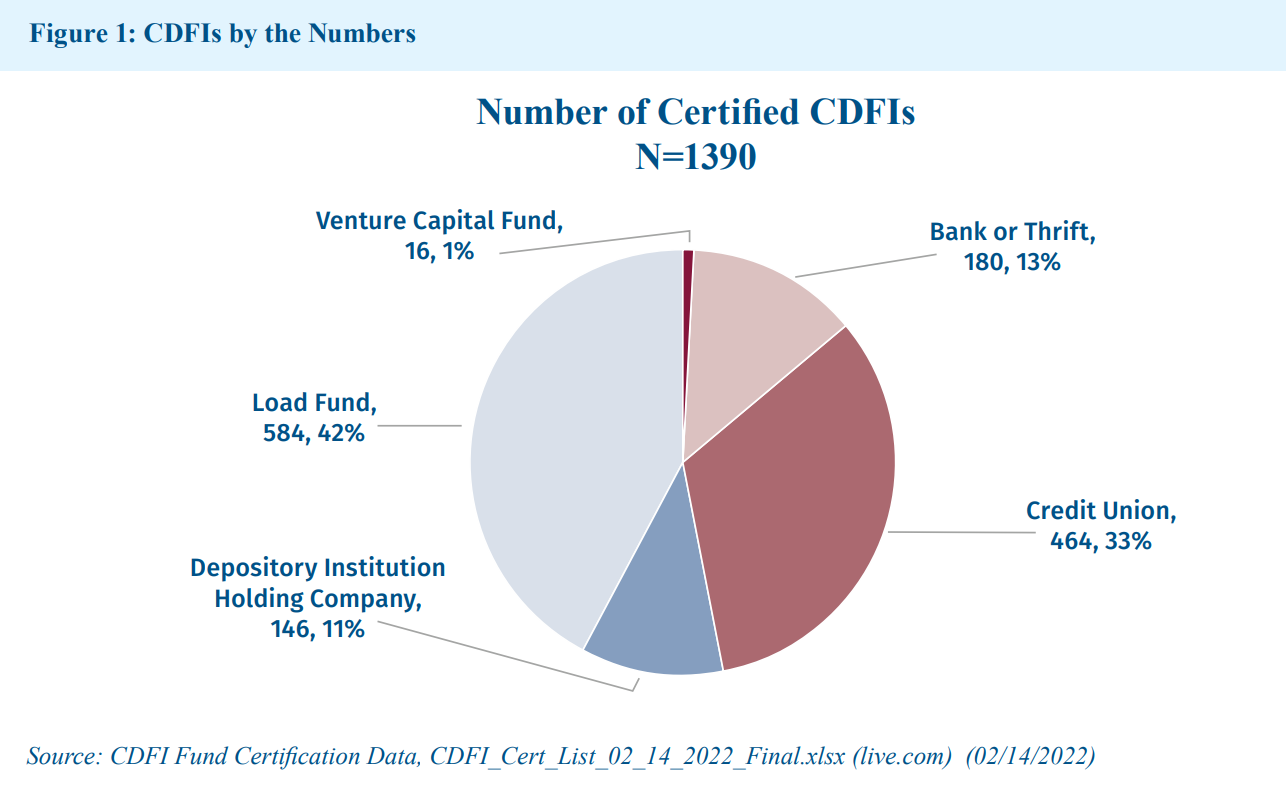

At first glance, the description of CDFI seems similar to how we discuss the credit union industry. Credit unions are cooperative financial institutions that are also mission-driven and aim to better the lives and financial position of members. For this reason, it should not be a surprise that credit unions make up a sizable portion (over one third) of current certified CDFIs. The figure below shows a breakdown of CDFIs by the type of institution, and shows that credit unions hold the second largest share of the pie, behind not-for-profit loan funds.

NCUA has encouraged credit unions to take advantage of the fact that many credit unions already operate in a manner that may qualify them for CDFI certification, and becoming certified comes with access to funding and resources that may otherwise take years to receive. In 2020 and 2021, a few CDFI targeted programs were created or expanded to counter the disparate effects of the pandemic on low-income and minority communities. These are just a few of the programs that offer funding or other resources for CDFIs:

- The CDFI Fund’s Small Dollar Loan Program launched in September 2021. This program supports reserves and creates additional cushion so CDFIs can maintain small dollar lending programs.

- The Treasury’s Emergency Capital Investment Program was created by the Consolidated Appropriations Act of 2021. This program provides federal funding for lending and expansion of services in low income and minority communities.

- The CDFI Rapid Response Program was created to quickly get funding to certified CDFIs through a streamlined application and review process.

- The Emergency Support and Minority Lending Program was also funded with the Consolidated Appropriations Act of 2021, and has not yet launched any services. The program was created primarily to increase investment in LMI minority communities.

As mentioned above, NCUA has encouraged credit unions to obtain CDFI certification, and worked with the CDFI Fund to simplify the process for credit unions. Low-income-designated credit unions can complete a streamlined application by registering in the NCUA’s CyberGrants system and completing the online forms. The NCUA’s Office of Credit Union Resources and Expansion will review each credit union’s products, services, and other indicators to determine whether the credit union qualifies for the streamlined certification process. Unfortunately, the streamlined application is being phased out, and our compliance team will keep an eye out for if and when it will reopen. Fortunately, credit unions can always apply for certification through the standard application process.