CFPB’s Report on Credit Card Late Fees

A few weeks ago, the Consumer Financial Protection Bureau (CFPB) published a report reviewing the trends in credit card late fees over the last few years. CFPB Director Chopra says, “many credit card issuers have made late fee penalties a core part of their profit model.” The report explains that late fees make up more than half of all credit card penalty fees and create a significant amount of income to credit card issuers.

In the report, the bureau spends a significant amount of time reviewing the impact to borrowers caused by excessive late fees. First, repeat late fees are typically higher than first time late fees, sometimes with an increase of $10-15. The bureau explains that this can be harmful to members with lower income and credit scores because they are more likely to make repeat late payments. The CFPB also explains that these members are much more likely to have subprime or deep subprime credit card terms, which are associated with higher interest payments and increased incidences of being charged a late payment.

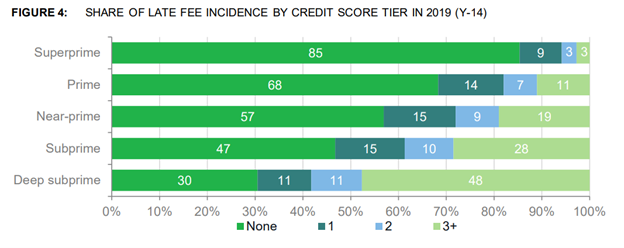

Here is one visual from the report, showing the frequency at which subprime credit card accounts were charged late fees in 2019. Contrarily, most above prime accounts went the calendar year without incurring a late fee.

The report also evaluates the burden of late fees on low income and minority communities. The bureau found that Black and low income communities paid significantly more in late fees in 2019. The bureau states the burden can be heavy for some members, noting “as consumers in poorer areas tend to carry smaller balances when they are late on a payment, the late fee they pay on top of a finance charge is typically a larger cost relative to their average daily balance.” Some credit unions have tackled this issue by offering credit-building products and budgeting services. These products help members with lower balances and weaker credit history to work their way up to better credit cards, while learning how to manage their funds.

Credit unions can also reduce the harm of excessive late fees by following all the rules in Regulation Z regarding penalty fees. As a reminder, section 1026.52(b) of Regulation Z requires a penalty fee to represent a “reasonable proportion of the total costs incurred” by the credit union as a result of the violation. In determining the costs incurred for a late payment, the commentary explains a credit union may look at the costs of collecting a late payment, notifying members of delinquencies and processing delinquencies in order to determine the appropriate amount of the late fee. The rule also provides a safe harbor for the dollar amount of penalty fees, which is updated regularly to account for inflation. Currently, these amounts are $30 for the first violation and $41 for a second violation within six billing cycles. The report found that credit card issuers stayed within the limits set by the regulation, although many issuers set fees near the maximum limits.

Regulation Z also creates notice requirements to ensure transparency between card issuers and members. Section 1026.6 describes the manner in which late fees and other penalty fees should be disclosed at account opening, and even requires this information be included in a table so that its easier to see. Credit card issuers may need to review their account opening processes to ensure all requirements are being met and members have a clear understanding of the costs associated with the account.

Although the burden of late fees can become a hinderance for some members, it is important for credit unions to continue to work with members to put them in appropriate and helpful credit products and continue to clearly identify the costs associated with each product.

Compliance professionals in the credit card space may want to read the full report for more insight from the bureau.