ICYMI: Recent Developments Involving Servicemembers

By: Reginald Watson, Regulatory Compliance Counsel, NAFCU

Greetings Compliance Friends!

When it comes to our beloved servicemembers, we often think about the years of physical and technical training, the physical dangers of deployment, and the courage of our volunteer troops. One often overlooked aspect of military life is the vulnerability that servicemembers and veterans face by predatory lending and other financial scams that specifically target them.

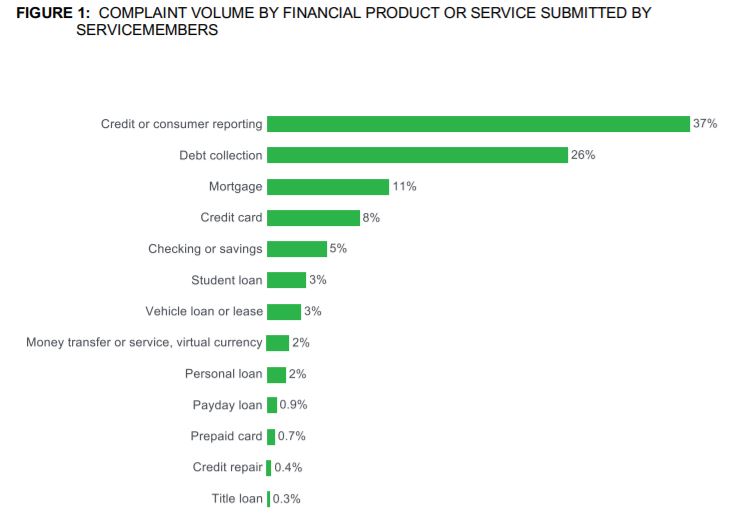

Last week, the Consumer Financial Protection Bureau (apparently back to the CFPB for now) released an annual report from the Office of Servicemember Affairs highlighting complaints submitted between April 1, 2017 and August 31, 2018, as well as CFPB enforcement actions related to the military community. The Dodd-Frank Wall Street Reform and Consumer Protection Act established the Office of Servicemember Affairs to help military families by addressing specific consumer protection concerns. Among several initiatives, the office is charged with monitoring servicemember complaints that are sent to the Bureau. Here is a chart from the report which breaks down more than 48,000 complaints received by the Bureau during the reporting period:

While I won’t get too into the weeds, a few evident trends did emerge. Credit or consumer reporting and debt collection were by far the most reported complaints, accounting for almost 64% of the total complaints submitted. This is not unlike some of the trends uncovered in the Bureau’s 2018 Complaint snapshot (covered in a previous blog). In addition to those general concerns, servicemembers are under particularly unique pressures as the Department of Defense (DOD) recently implemented new security clearance rules which continuously monitor servicemembers’ credit histories. The majority of consumer reporting complaints involved potentially incorrect information on the credit or consumer report followed by problems with investigations into these inaccuracies. Almost half of the debt collection complaints revolved around attempts to collect a debt that the servicemember believes he or she did not owe. Servicemember complaints also covered things like mortgages, credit cards, student loan servicing, and automobile loan-financed add-on products, such as guaranteed asset protection (GAP insurance).

For credit unions with a large representation of the military in their member base, it may not be a bad idea to pay particular attention to assisting these members and quickly handling complaints related to consumer reporting as it may now have a more serious impact on their security clearance and ability to serve our country. A significant number of complaints received about a particular credit union may also open the credit union up to greater regulatory scrutiny. Given the Bureau’s most recent request for clear authority from Congress to supervise for compliance with the Military Lending Act, it is possible that this may also become an increasing area of focus over the next year if the CFPB were granted express supervisory authority.

It seems this focus on servicemembers may already be in the works. Earlier last week, the Bureau also issued a consent order against a (former) contract broker for illegal lending practices that targeted veterans by offering lump sum payments at an egregious interest rate in exchange for the right to receive a portion of a veteran’s pension. Since enforcement actions have mostly slowed down under the current administration, this recent consent order may be further evidence that the CFPB is more closely examining complaints involving the military, both active duty and veterans.

For compliance with the Military Lending Act, NAFCU members may download our currently available MLA-related resources including our comprehensive MLA Guide here.