Bureau New Releases: Complaint Snapshot; HMDA Filing Instructions Guide

By: Reginald Watson, Regulatory Compliance Counsel, NAFCU

Greetings Compliance Friends!

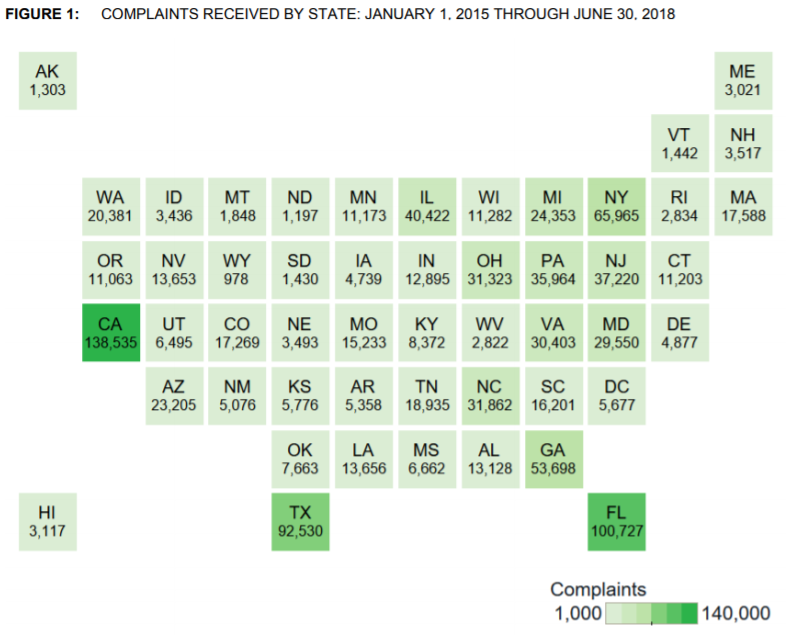

Not quite on par with the latest iPhone announcement, the Bureau recently released its Complaint Snapshot: 50 States Report, which provides a helpful analysis of all complaints received between January 1, 2015 and June 30, 2018. While there has been plenty of political jostling recently about how the Bureau uses the complaint database and what information it makes public, we hope it doesn’t lead to this:

The report itself provides a state-by-state analysis of the complaints received in descending order by the number of complaints submitted per 100,000 people. The report begins with a breakdown of the total complaints received by state. Unsurprisingly the states with some of the largest populations seem to lead the way:

While we won’t get too in the weeds on any particular state's data, a few evident trends did emerge. Debt collection and credit/consumer reporting were by far the most reported complaints, appearing as the top two issues in all but two states. The next two most complained about topics seem to be in the general areas of mortgages and credit cards.

When it comes to debt collection, the most reported issue is described as “attempts to collect debt not owed.” Consumer credit reporting tends to go hand in hand with debt collection efforts and the specific issue most reported there is described as “incorrect information on your report.” While it is not entirely clear to what extent, if any, these results will form the basis of any proposed rulemakings in the near future, it may reflect the Bureau’s Supervisory Highlights released this past summer which provided some general information about supervisory findings in the debt collection context. We previously blogged about some of the other supervisory highlights here.

In the debt collection section of the Supervisory Highlights, the Bureau found several issues with creditors and debt collectors who did not properly respond to debt verification requests prior to continuing debt collection efforts. While the definition of a debt collector under the Fair Debt Collection Practices Act (FDCPA) does not typically apply to credit unions collecting their own debts, the Bureau has previously indicated that many of the practices prohibited by the FDCPA may still be considered unfair, deceptive, or abusive acts or practices in violation of the Consumer Financial Protection Act. See, CFPB Bulletin 2013-07. See also, FDCPA, 15 U.S.C. § 1692a(6). Thus, it may not be a bad idea to review your credit union’s debt collection and credit reporting procedures to ensure they address responding to debt verification requests and ensure accurate reporting of valid debts, as this may increasingly become an area of focus for the Bureau. For additional information on the Fair Credit Reporting Act’s accuracy and integrity standards, NAFCU members may wish to refer to this Compliance Monitor article, A Furnisher’s Guide to the FCRA.

***

HMDA Filing Instructions Guidance

This past week, the Bureau also released a new Filing Instructions Guide for HMDA data collected in 2019. The guide provides technical instruction on filing data collected in 2019 and reportable in 2020 so that credit unions may get a head start on updating their policies and procedures. NAFCU is reviewing the guide and making note of the changes. For all things HMDA related, check out NAFCU’s HMDA landing page and this blog, as well as our free HMDA Update Webinar from a few weeks ago featuring members of the BCFP.

Finally, please remember that as far as the NAFCU Compliance team is concerned, we prefer questions over complaints!