Artificial Intelligence: A Frontier Worth Exploring for Your Credit Union

By: Larry Pruss, Strategic Resource Management

[Blog post 1 of 2]

Artificial intelligence, or AI, may sound overwhelming or even scary. The truth is it can both automate and improve services delivered to members while improving the bottom line of financial institutions.

AI is training computers to do things humans currently do better. Machines, using complex mathematical algorithms, demonstrate at least some behaviors associated with human intelligence. AI is often used in automating repetitive tasks, but automation and AI are very different solutions. AI covers a broad range of technologies including robotics, image and voice recognition.

AI can be automatically improved by adding components of machine learning. Machine learning is an application of AI that provides the system the ability to automatically learn and improve from experience, much the way a child learns from his or her environment.

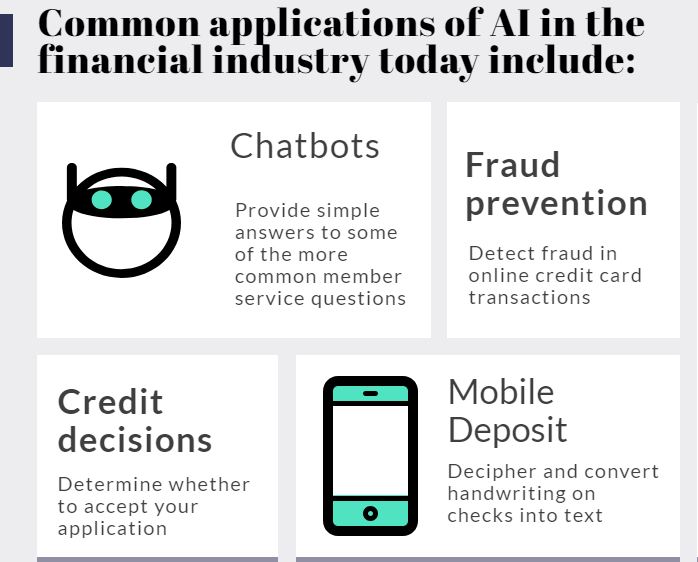

Common applications of AI in the financial industry today include:

- Chatbots – Chatbots are being deployed to provide simple answers to some of the more common member service questions. Depending on a series of questions and member responses, the AI figures out the most appropriate course of action.

- Mobile Deposit – Most large financial institutions and even smaller ones offer the remote deposit capture through consumers’ smartphones. The vast majority of these rely on AI to decipher and convert handwriting on checks into text via optical character recognition.

- Credit decisions – Whenever you apply for a loan or credit card, financial institutions must quickly determine whether to accept your application and if so, what specific terms, such as interest rate and credit limit, to offer. FICO uses machine learning both in developing a consumer’s FICO score, which nearly all financial institutions use to make credit decisions, and in determining the specific risk assessment for individual customers. MIT researchers found that machine learning could be used to reduce a bank’s losses on delinquent members by up to 25%.

- Fraud prevention – Machine learning is used for detecting fraud in online credit card transactions. Fraud is the primary reason online payment processing is more expensive for merchants than in-person transactions.

Listen to the recent podcast, "Exploring Artificial Intelligence."

AI is very good at seeing patterns in the data. Judgement, and in particular judgment decisions that may have an ethical component, however, can be problematic. We’ve all been faced with making a decision that might positively impact a member’s life but, would do so at some risk to our financial model. Are you ready for AI to be making those decisions? Maybe, maybe not.

So where is AI heading? Does it evolve into super-intelligence, where it surpasses humans? If so, can we avoid passing on human traits, such as bias? Remember, your members are using AI every day when they ask Alexa or Siri for the weather. Your credit union can augment its employees and members’ experience with AI as well.