By Curt Long, Chief Economist and Vice President of Research, NAFCU

There are plenty of lessons to learn from the Great Recession. For the Federal Reserve, one thing that became clear early on was that traditional policy tools would be inadequate to provide an appropriate level of monetary stimulus. Central banks around the world opted for an unproven method: large-scale asset purchases.

Quantitative easing was not without its critics. Many expected a spike in inflation, which never materialized. There was broader concern that efforts to manipulate financial markets would lead to increased volatility and asset bubbles. And at a minimum, shouldn’t the economic benefits of temporarily bloating the Fed’s balance sheet do similar-sized damage to the economy when the balance sheet is normalized?

Although there is disagreement as to the benefits of quantitative easing (QE), most believe it was at least modestly successful in lowering long-term rates and stimulating economic growth. However, estimates of the downside of the maneuver are that the costs were trivial. Even speculation around the likelihood that restoring the Fed’s balance sheet (aka quantitative tightening or QT) might restrict growth have fallen out of favor. In considering how the next recession might play out, it is clear that the Fed has added QE to its playbook.

An Asymmetric Outcome

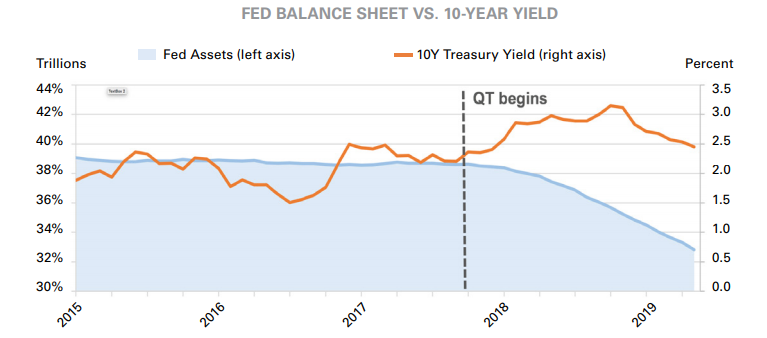

If there is one phrase the Fed has used most often to describe QT, it is “in the background.” Multiple Fed chairs have downplayed the expected impact of QT on interest rates and financial markets. So when yields on 10-year Treasuries drifted upward following the onset of QT in October 2017 (see “Fed Balance Sheet vs. 10-Year Yield”), it seemed to contradict those reassurances. Many fretted that unwinding QE was reflating interest rates and potentially squelching economic growth. But since that time, rates have declined, even as the Fed’s balance sheet continues to downsize.

The Fed’s view is that the respective impacts of QE and QT are not symmetric. James Bullard, president of the Federal Reserve Bank of St. Louis, recently outlined the reasons behind that belief. Fed researchers found that increasing the size of banking sector reserves on the Fed’s balance sheet beyond a minimal threshold only has an impact on financial intermediation and credit spreads (and, hence, the broader economy) when interest rates are near zero. Therefore, the three rounds of QE acted to stimulate the economy because rates were already at zero. However, now that they are comfortably above that level, QT can operate with few economic ramifications.

Another consideration involves the Fed’s communication strategy. In reflecting on the impact of QT, many have seized on the idea that the most tangible impact it had was adding credibility to the Fed’s stated intentions to keep interest rates historically low for such a long period. There are some, in fact, who see this signaling effect as being the only practical way in which QE affected the economy.

However, as Ben Broadbent, deputy governor of the Bank of England, pointed out, the Fed’s communications around QE and QT were quite different. In embarking upon QE, former Fed Chair Ben Bernanke made it clear that it would act as an “addition” to the Fed’s stimulative interest rate policy. But the Fed has consistently communicated to financial markets that QT would have little impact, and it would not represent a device for enacting monetary policy. In doing so, reductions to the Fed’s balance sheet do not carry the same signal about the Fed’s intentions to adjust interest rates.

The Next Go-Round

The Federal Reserve has clearly formed a favorable view of large-scale asset purchases, and in their ability to positively influence the economy during troubled times without unduly damaging it when those actions are unwound. Since most expect rates to stay far closer to zero than they have been throughout the Fed’s history, it seems likely that QE will play prominently in the Fed’s response to the next recession. One important implication for credit unions is that, with QE, the Fed believes it has a tool to flatten the yield curve. Those conditions are widely believed to be difficult on financial intermediaries such as banks and credit unions, particularly small ones. This could make the next recession a more difficult one to survive for many institutions.

This article was published in the July-August 2019 edition of The NAFCU Journal magazine.

Want to receive The NAFCU Journal in your inbox? Update your email preferences.

Related Content

- The Bottom Line: The Phillips Curve, by Curt Long in the May-June 2019 edition of The NAFCU Journal magazine

- NAFCU’s Economic and CU Monitor (member-only)