By Curt Long

We are officially in the midst of the longest U.S. economic expansion in history. Beyond its durability, the recovery has been highlighted by a number of achievements, such as a sub-4 percent unemployment rate and a booming stock market. Yet most economists believe that the recovery has been a tepid one, in which real GDP growth has generally failed to break 3 percent and wage growth has been muted. Many observers are now blaming the Federal Reserve for committing its hallmark sin of raising rates too soon and too quickly, squelching growth in the process.

Inflation underlies these claims. The Fed aims for year-over-year inflation of 2 percent, yet only on two brief occasions over the past 10 years has it achieved that target. At the Fed’s annual August seminar in Jackson Hole, Wyo., Chairman Jerome Powell stated that “low inflation has been the main concern for the past decade.” Critics, including some members of the Federal Open Market Committee, which sets the Fed’s monetary policy, assert that the committee has treated the 2 percent target as a ceiling. As inflation starts to approach its target, the committee tightens policy prematurely, which has caused consistent downside misses in price growth. Many who hold this view would say that the relationship between resource utilization and inflation has weakened, yet the Fed has been slow to pick up on it. If true, policymakers have substantially greater latitude to maintain low rates and stimulate growth without risking a rise in prices.

A different view of inflation is laid out in the June 2019 research paper “Slack and Cyclically Sensitive Inflation” by James Stock of Harvard and Mark Watson of Princeton. The pair disaggregates the components of inflation into those that are historically sensitive to the business cycle (or “cyclical”) and those that are not (“acyclical”). The researchers theorize that a leading cause for acyclical inflation is that some products are either priced in global markets (such as commodities) or have prices that are difficult to measure (such as financial services). A 2017 study by the Federal Reserve Bank of San Francisco highlighted the role of health care costs, which are often negotiated by health care providers and subject to legislative actions. Each study finds that acyclical elements account for roughly half of overall measures of inflation.

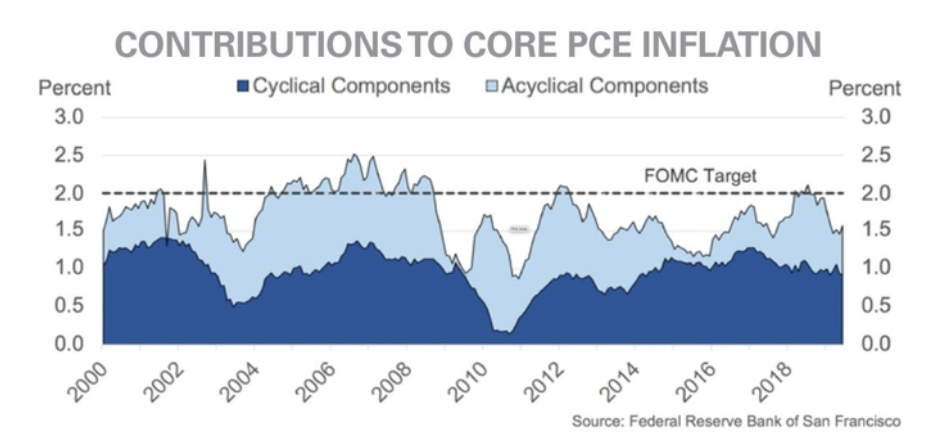

If these findings are valid, and if policymakers are searching for the amount of “heat” generated by the economy in the form of price pressures, the cyclical elements are most relevant. The accompanying chart, published by the Federal Reserve Bank of San Francisco, shows a disaggregation of year-over-year inflation into cyclical and acyclical components.

Since each accounts for roughly half of the overall basket of goods in the consumption expenditures index, a 1 percentage point contribution to overall inflation from cyclical components is consistent with 2 percent overall inflation, on average. Over the decade-long expansion, cyclical inflation has met or exceeded this mark in 80 months, while acyclical inflation has done so in only 11 months. The shortfall in inflation, therefore, appears to be largely the result of noneconomic factors impacting those acyclical elements.

The title of this year’s Jackson Hole symposium was “Challenges for Monetary Policy,” and the topics of many of the presentations focused on the inability of central bankers to achieve employment and inflation mandates using their traditional toolbox. Some are even wondering whether the entire interest-rate targeting framework needs to be scrapped. Yet it may be that the Fed has been able to produce enough heat to meet both sides of its dual mandate, even if it hasn’t felt like it. Maybe they just have their hands in the wrong place.

Curt Long is NAFCU’s chief economist and vice president of research.

This article was published in the November-December 2019 edition of The NAFCU Journal magazine.

Want to receive The NAFCU Journal in your inbox? Update your email preferences.

Related Content

- The NAFCU Journal: Growing the Fed’s toolbox

- NAFCU's Macro Data Flash Report: Federal Open Market Committee (member-only)

- Economic & CU Monitor: Economic outlook (member-only)