Newsroom

Fed report: Credit card balances fell $49B in Q1

A new report from the Federal Reserve Bank of New York found that credit card balances saw the second largest quarterly decline in history, falling $49 billion during the first quarter of 2021. The Quarterly Report on Household Debt and Credit looks at several sectors, including mortgages, auto lending, and student loans.

A new report from the Federal Reserve Bank of New York found that credit card balances saw the second largest quarterly decline in history, falling $49 billion during the first quarter of 2021. The Quarterly Report on Household Debt and Credit looks at several sectors, including mortgages, auto lending, and student loans.

Related to credit card balances, the report also noted that they are $157 billion lower than at the end of 2019, "consistent with both paydowns among borrowers and constrained consumption opportunities."

"2021 began with a strong increase in new extensions of mortgage and auto loan credit coupled with a substantial drop in credit card balances," said Andrew Haughwout, senior vice president at the New York Fed. "However, surging retail sales volumes suggest that a combination of stimulus checks, increased consumer confidence, and pent-up demand are both supporting consumption and also helping borrowers reduce revolving debt balances."

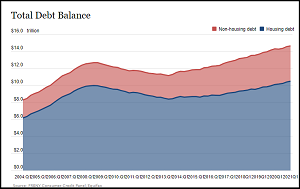

Mortgage balances, which are the largest component of household debt, rose $117 billion in the first quarter and stood at $10.16 trillion at the end of March. Auto and student loan balances also increased $88 billion and $29 billion, respectively, during the quarter.

Mortgage originations and new auto loans were strong during the first quarter. The Fed's report also found that aggregate delinquency rates across all debt products have continued to decline since the start of the coronavirus pandemic, likely attributed to forbearance options offered in relief packages and by lenders.

Access the full report here. Member credit unions can also access NAFCU's analysis into economic trends related to home, retail, auto sales, and more here.