Newsroom

How will debt collection proposal affect CUs?

As the CFPB considers a rulemaking related to third-party debt collection, NAFCU would like to know how it could impact credit unions that use third-party vendors or credit union service organizations (CUSOs) to collect debts owed.

As the CFPB considers a rulemaking related to third-party debt collection, NAFCU would like to know how it could impact credit unions that use third-party vendors or credit union service organizations (CUSOs) to collect debts owed.

Although rulemakings for both first- and third-party debt collection were initially contemplated, the bureau’s focus shifted to just third-party. However, a first-party debt collection rule is still possible in the future. NAFCU previously urged the bureau to exempt credit unions from any rules related to first- and third-party debt collection, as credit unions are not the bad actors in this space.

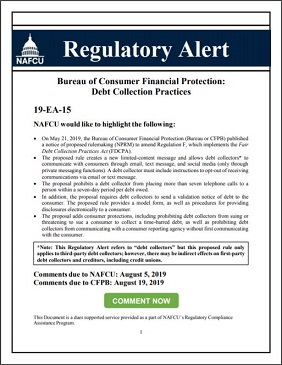

In a Regulatory Alert sent to member credit unions Thursday, NAFCU outlined that the proposal would:

- create a new limited-content message and allow debt collectors to communicate with consumers through email, text message and social media (only through private messaging functions), though the debt collector must include instructions to opt-out of receiving communications via email or text message;

- prohibit a debt collector from placing more than seven telephone calls to a person within a seven-day period per debt owed;

- require debt collectors to send validation notice of debt to the consumer; and

- add consumer protections, including prohibiting debt collectors from suing or threatening to sue a consumer to collect a time-barred debt and from communicating with a consumer reporting agency without first communicating with the consumer.

The association would like to know, among other things, if credit unions that use third-party vendors to collect debt are concerned about liability, would face increased compliance costs or burdens and would have to update internal policies and procedures related to opt-out notices.

Credit unions can submit feedback on the proposal to NAFCU through its Regulatory Alert until Aug. 5; comments are due to the CFPB Aug. 19.