Strengthening communications and internal controls can help lessen the heightened risk of lawsuits due to economic uncertainty

By M. Diane McCormick

In financial services, lawsuits are a fact of life. However, for many small and midsize credit unions, the risk has traditionally come from individual members filing claims over their personal disputes.

Now, a changing litigation landscape is putting credit unions of all sizes at risk of costly class-action lawsuits. Missteps and miscommunications by financial institutions have always been fruitful ground for plaintiffs’ attorneys seeking big payouts, and a pandemic-related downturn sows the kind of confusion that feeds a class-action environment.

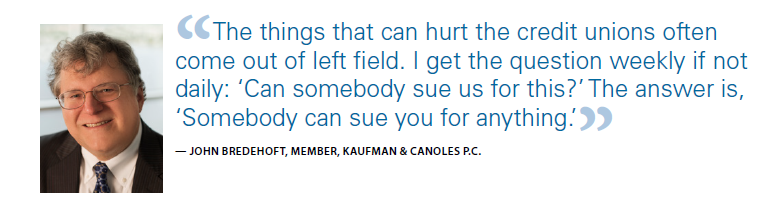

"The things that can hurt the credit unions often come out of left field,” says John Bredehoft, member of Kaufman & Canoles P.C. of Norfolk, Va. “I get the question weekly if not daily: ‘Can somebody sue us for this?’ The answer is, ‘Somebody can sue you for anything.’”

In a world where overdraft policies, remote deposit capture (RDC), Fair Credit Reporting Act (FCRA) compliance and privacy laws can attract litigation, risks are heightened by economic uncertainty. Credit unions can harden their defenses by strengthening their communications and internal controls, and by documenting the decisions made as they conduct business during rapidly shifting circumstances.

Overdraft

"Overdraft policies constitute the biggest area of litigation activity that NAFCU is witnessing among credit unions and throughout the financial services sector", says Carrie Hunt, executive vice president of government affairs and general counsel for NAFCU. One round of class actions is questioning whether credit unions can perform certain activities based on the terms of their account agreements. "Courts are approaching the cases differently," Hunt says. In some cases, they are reviewing only the underlying contractual disputes. In others, they are considering the obligations put on credit unions under the Consumer Financial Protection Bureau’s Regulation E, its rules pertaining to account agreements.

“These lawsuits are quite varied,” Hunt says. Plaintiffs and plaintiffs’ attorneys “are trying to grasp any potential issue to claim these consumers weren’t put on notice.”

"Overdraft complaints can be fueled by the complexities of posting and processing transactions, making them hard to explain in agreements," says Hal Scoggins, attorney at Farleigh Wada Witt in Portland, Ore. Add to that an “innate distrust of financial institutions,” he says, and plaintiffs’ attorneys can easily find potential plaintiffs for threatened class-action suits. “Those can be incredibly time-consuming and difficult to defend, even if the credit union is doing absolutely everything right.”

"One common lawsuit involves claims of a credit union charging overdraft fees when a member’s debit card transaction is approved and intervening transactions by debit card, check or withdrawal leads to a negative balance when the debit card transaction clears later," Scoggins says. "In another, credit unions have been accused of charging returned-check fees at the initial presentment and also when the payee sends the check through a second time. Claimants say the practice is inconsistent with disclosures that provide for a fee charged “per item.”

“There’s going to be a shakeout period where we start to get rulings from the courts on those two particular claims, and that will dictate what happens in the next wave — whether this wave dies out, or whether plaintiffs encouraged by positive rulings continue filing and ramp up their efforts,” Scoggins says.

In recent years, Bredehoft has seen hopeful signs in the clarity of account agreements. Although agreements are longer, “we’re seeing them written in extraordinarily plain English, with words of no more than two syllables, that would be virtually impossible to read and misunderstand.”

FCRA AND COLLECTIONS

"The Fair Credit Reporting Act requires that financial institutions report consumer credit information accurately and fairly. However, the Consumer Data Industry Association’s rules for those actions are too intricate and detailed for most industry outsiders to comprehend, Scoggins says." “Even a lot of people in the industry don’t understand them.”

When a credit union sends an outstanding loan to a collection agency, any misalignment in reporting — or even properly performed filings — can create the appearance that the debtor owes two obligations instead of one.

“Someone who knows credit reporting knows the fact of the matter, but the plaintiff's attorney doesn’t know, so they might sue the credit union for inaccurate reporting they claim is damaging the person’s credit score,” Scoggins says.

Another collection-based concern involves claims related to collection practices under state laws applying to financial institutions. Some plaintiff s’ attorneys are claiming that a financial institution’s practices that would have violated the Fair Debt Collection Practices Act, which applies only to third-party collectors, is evidence that the organization violated state consumer protection or deceptive practices acts.

"Most credit unions have mastered core compliance with FCRA, but paying attention to its breadth is necessary," says Bredehoft. All pieces of information relating to a person’s creditworthiness or reputation are covered, demanding a broad view of sufficiency in internal controls.

“Gossip is covered,” he says, “and I don’t see many organizations with gossip policies.”

REMOTE DEPOSIT CAPTURE

Remote deposit capture has become a banking mainstay, as familiar to digital-first consumers as online payments. Credit unions have adopted RDC through vendors or developed their own systems. However, the long-running patent dispute between USAA and technology developer Mitek over a key technology remains unsettled. The dispute encompassed other financial institutions, with recent court rulings requiring Wells Fargo to pay USAA hundreds of millions of dollars for its use of several patents, but litigation among the various parties continues.

Could credit unions find themselves being sued for using the character-recognition software at the heart of the dispute? Those that have incorporated the technology into systems developed in-house could be sued directly — which was the case with Wells Fargo — or pressured into license agreements.

Hunt recommends that credit unions using vendors review their contracts and consider developing indemnification clauses to help shield them from lawsuits. They could also prepare contingency plans, in case they can no longer use the technology in their RDC systems.

“Clearly, credit unions want to be able to continue to offer remote deposit capture, and we’ll have to see how that litigation plays out,” Hunt says. “The problem is, until the litigation is resolved, they will never fully know the answers as to whether or not these systems are set up appropriately, so we have got to see this through.”

FUTURE ISSUES

"New state-level data privacy laws enacted or pending could raise the potential of lawsuits," Hunt says. Under the federal Gramm-Leach-Bliley Act (GLBA), credit unions must explain how they share and protect consumer information. However, the U.S. lacks a comprehensive federal data privacy standard, and states are stepping into that gap.

California leads the trend with its California Consumer Privacy Act, which took effect in January. As NAFCU noted in its “NAFCU’s Principles for a Federal Data Privacy Standard,” a piecemeal approach could compel credit unions to comply with multiple state privacy laws.

“Credit unions of all sizes are beginning to understand the massive systems overhaul necessary to comply with potentially 50 different laws as well as the potential legal implications of violating these laws,” the brief states in its call for a uniform national standard that preempts state privacy laws.

The California law does not cover information that is subject to the federal Gramm-Leach-Bliley Act. “Different people will argue about how much of the information the credit union has is subject to Gramm-Leach-Bliley, but most are covered,” Scoggins says. “That makes financial institutions less of a target for class-action attorneys right now.”

COMMUNICATIONS

Credit unions have a two-part strategy to deploy in warding off litigation, especially cases involving consumer agreements. “No. 1, say what you do; and No. 2, do what you say,” Scoggins says.

Adhering to that rule requires joint attention on communications and training.

On the communications side, he says, “agreements should be clear, they should be complete, and they should actually describe what you’re doing in a way that consumers can understand.”

With their community-service missions, credit unions typically admit any mistakes they uncover and do what they need to do to make it right for members. “In the vast majority of cases, that leaves the member happy,” Scoggins says. If the credit union disputes a claim, “that’s OK, too. Respond that we’re in the right, and here’s why, and here’s why we’re not going to do what you wanted.”

"Internal controls are essential for carrying out agreements to the letter because most mistakes are caused by someone who didn’t understand the policy," Bredehoft says. Control means having someone in charge of making sure that everyone who serves the member knows the agreement backward and forward, and anyone involved with credit reporting knows the FCRA backward and forward.

DISRUPTED WORLD

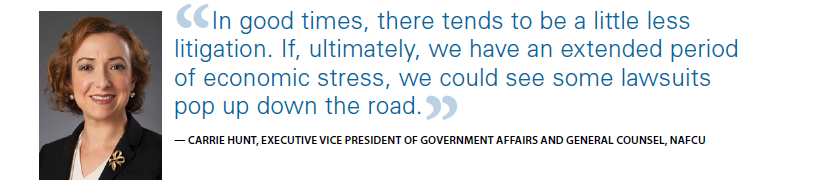

When the economy goes down, lawsuits go up. As such, the disruptive COVID-19 crisis is certain to be felt in the litigation landscape. “In good times, there tends to be a little less litigation,” Hunt says. “If, ultimately, we have an extended period of economic stress, we could see some lawsuits pop up down the road.”

Bredehoft agrees that “when the economy slows down, the sharks circle.” Plaintiff s’ attorneys will look for minor technical changes in laws that institutions might not have implemented. Plus, financial institutions are suddenly confronting the legal repercussions of issues they’d never had to address before — such as whether to bar someone who appears ill from entering a branch, or how to give lunch breaks to employees who can’t leave the building.

“We’re going into so many unseen fields,” Bredehoft says. “We haven’t been preparing for them, and working through these matters is difficult.”

"New laws, regulations and rules that contradict one another present a major challenge in the COVID-19 era," Bredehoft says. He advises that credit unions make every decision with an eye on the future, documenting the rationale for each one. “Not 20-page memos, but at least memorialized in an email that is permanent, because that kind of thinking is hard to re-create afterward.”

"As more credit unions become susceptible to class actions, an increasing number are considering arbitration clauses in their member and account agreements," Scoggins says. The idea of prohibiting class-action suits might have once seemed antithetical to credit unions, but “now we’re seeing that tide turn.”

Arbitration clauses have pros and cons. They can help ward off class-action cases but, unlike lawsuits, arbitration decisions can’t be appealed. Plus, arbitration can be expensive, and in some circumstances, attorney fees are not recoverable.

“It’s a very specific analysis and risk-benefit analysis that each credit union has to make carefully after talking with their attorneys,” Scoggins says.

Bredehoft warns that pandemic-inspired good deeds can have unintended consequences. During the pandemic, many credit unions are easing their terms and policies, perhaps suspending repossessions or lifting mortgage payment requirements for a period.

However, without careful legal review, documents presenting the policies could yield essential powers beyond the crisis parameters.

“You don’t want to give up all right ever to collect money on the mortgage,” says Bredehoft. “You need precise legal wording in some states when you make modifications. Getting that kind of focused advice can keep you out of trouble that can cost so much more later.”

In the suddenly disrupted economy, it’s not only the large credit unions that should constantly scan the horizon for litigation risk. The credit union industry's relative health means that small and midsize institutions could appear on the radar of plaintiff s’ attorneys seeking new targets.

“Litigation risk,” says Hunt, “is something all credit unions have to face and address.”

M. Diane McCormick is a freelance journalist and a frequent contributor to The NAFCU Journal.

This article was published in the July-August 2020 edition of The NAFCU Journal magazine.

Want to receive The NAFCU Journal in your inbox? Update your email preferences.

Related Content:

- The NAFCU Journal: Advocacy Minimizes Risks

- Compliance Hot Topic: Overdraft Litigation

- Compliance Blog: Litigation Risk Update – Indirect Lending and FCRA

- Compliance Monitor: Remote Deposit Capture Patent Litigation Update (member-only)