By Robert Bittner

Banking is so much more complicated than when I started in this industry in the ’70s,” says Cindy Wanamaker, chief operations officer and executive vice president of Franklin Mint Federal Credit Union, which covers the greater Philadelphia region. “More regulations, more fraud, electronic services that never even existed in the past. There is more to know, more to remember, and more to double-check in the back office.”

It is the mission of the National Credit Union Administration (NCUA) to help manage that complexity through supervision, regulation, and insurance. Fundamental to the agency’s work is the NCUA exam, during which examiners will devote days — or even weeks — to reviewing and investigating critical phases of a credit union’s operation, validating regulatory compliance while alerting the credit union and its team to existing and potential problems requiring corrective measures.

Like an annual physical exam at the doctor’s office, not every NCUA exam is pleasant or painless. Yet everyone can provide valuable insight into a credit union’s processes and people — information that will only strengthen a credit union’s ability to serve its community. In that way, NCUA examiners can be vital partners in a credit union’s overall success.

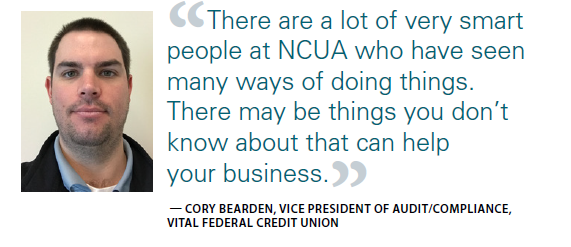

“Partnership should be the mindset” when preparing for an NCUA exam, says Cory Bearden, vice president of audit/ compliance at VITAL Federal Credit Union in Spartanburg, S.C., and a former NCUA examiner. “There are a lot of very smart people at NCUA who have seen many ways of doing things. There may be things you don’t know about that can help your business.”

Before the examiners arrive, however, there is value in knowing as much about your business as possible.

The Internal Audit

“As part of an NCUA exam, your examiners will often start with the credit union’s own internal audit reports,” Wanamaker says. A credit union’s audit gives examiners a sense of what the institution has already assessed as well as the areas it has already identified as needing improvement. “NCUA exams are a point in time,” Wanamaker continues. “The internal audit shows diligence all year long.

“The audit function can be handled by an internal staff auditor, or it can be outsourced; due to the diversity of knowledge that’s needed, it can be difficult to have internal staff with a full knowledge base,” she notes. At FMFCU, they outsourced that function when their auditor retired. “The outside auditors focus on operational compliance areas — lending, loan servicing, deposit services, TRID, Reg Z, Reg E, courtesy overdraft, etc.,” she says. Those reports are presented to the supervisory committee throughout the year, demonstrating that the credit union considers compliance and internal controls to be critical parts of its overall operations.

“Internally,” Wanamaker continues, “every department also has quality-control aspects to cover in their individual business units. Mistakes happen — especially when you have member-facing staff who are ‘jack-of-all-trades’ — and having a strong quality-control process catches them, hopefully, before they negatively impact members.”

In Bearden’s experience, credit unions that had done their internal homework fared better. “We seemed to see a correlation between financial success and those credit unions that knew their own performance metrics — and those of their peers.”

Priority Management

Each year, the NCUA releases a list of “supervisory priorities” that highlights key areas on which examiners will concentrate their attention. These priorities are linked to areas of highest risk, new products and services, and compliance with new or amended federal regulations. In 2019, those priorities included Bank Secrecy Act (BSA) compliance, Current Expected Credit Losses (CECL), and information systems and assurance. Along with the list of priorities, the NCUA provides links to support resources and an online version of the agency’s examiner’s guide for reference. “The supervisory priorities are essentially a heads-up, so there aren’t any big surprises,” Wanamaker says.

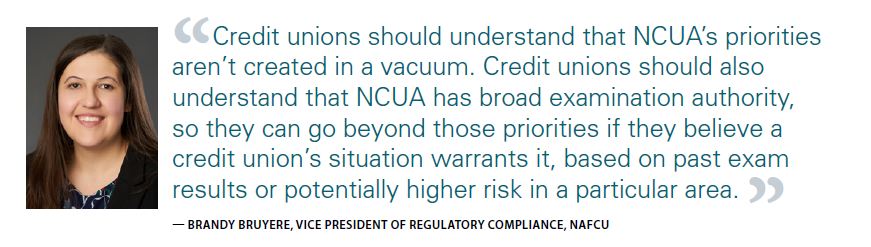

Brandy Bruyere, NAFCU’s vice president of regulatory compliance, says that these priorities, though they shift over time, are not random. “Credit unions should understand that NCUA’s priorities aren’t created in a vacuum,” she says. But focusing only on the published priorities of a given year is a mistake. “Credit unions should also understand that NCUA has broad examination authority, so they can go beyond those priorities if they believe a credit union’s situation warrants it, based on past exam results or potentially higher risk in a particular area.”

For example, Wanamaker points out that a number of credit unions now are going through core system conversions. That situation may lead examiners to request reports that would not have come up otherwise. “If you’re in that situation,” she says, “before you get off that old system, anticipate what might be needed for the exam so you can run reports and have them when the examiners visit. And be prepared for a more granular exam than you may have had in the past. Because we had recently gone through a core conversion, I think the examiners dug a little bit deeper to make sure everything moved over correctly.”

Welcome, Partners

Most credit unions are welcoming and responsive to the exam team, Bruyere says, and that gets the process off on the right foot. “But if you’re getting a request [from an examiner] and it’s not clear why or what the goal is, don’t be afraid to ask why that particular request has been made,” she says. “Try to have as good and open a dialogue as possible.”

From his experience, former NCUA examiner Bearden recalls that the smaller the credit union is, the more nervous they tend to be about the exam. “The burden is on the examiner to communicate [any] issue in a way conducive to problem-solving,” he says. “For me, it was pretty simple: I don’t want to argue with people or have a difficult day-to-day job. It’s important for everyone to trust each other.”

To help the relationship get off to the best start, officials with the NCUA’s Office of Examination and Insurance advise that, when possible, management should meet with the examiner-in-charge (EIC) and the exam team at the outset of each exam. This provides opportunities for the team to meet the key staff members they’ll be working with, NCUA officials say.

In addition, NCUA recommends several steps that can help to manage the exam process:

- Have the items that were included on the “items needed” list provided by NCUA pulled and ready for the exam team when they arrive. NCUA examiners are required to provide management with this important list well in advance of the on-site fieldwork, and to tailor the list to what is really needed for examining a particular credit union.

- Schedule regular update meetings with the EIC — daily, if possible.

- Request that the EIC meet with the board of directors following an exam and provide timely feedback regarding draft Documents of Resolution (DOR), examiner findings, loan exceptions and other documents related to the exam.

“Your role as an examiner is not necessarily defined for you by the agency,” Bearden says, “so every examiner sees it differently. I saw myself as a representative of the credit union to their regulator, and vice versa. Of course, my primary focus was on meeting NCUA’s requirements. But if a credit union had feedback regarding something, I saw it as my duty to take that on. I also wanted to be open to asking if we as an agency were doing things that were holding a credit union back. I tried to make the most of the authority I did have.”

NCUA’s Office of Examination and Insurance officials say they’ve found that credit unions that work closely with their EIC and exam team report a more positive experience, and they appreciate a management team that communicates early and often.

Improving the Process

Of course, not every interaction or every exam can occur without issues.

“Different examiners have different priorities,” Bearden says, “and that leads to inconsistency among examiners. It’s particularly evident among smaller credit unions because the agency tends to assign them to younger, less-experienced examiners. And then there can be inconsistencies between how an examiner handles different credit unions within a region. When I needed to take corrective action, my No. 1 priority was to be consistent between credit unions. If you’re not, that gets around, and you lose credibility.”

Three years ago, the NCUA itself highlighted the need to improve examiner consistency and knowledge in a 2016 NCUA Report submitted by then-NCUA Board Chairman Rick Metsger. Metsger wrote: “Additional examiner training and development will help address examiner consistency concerns raised by credit unions. Our examiner training will continue to emphasize the importance of timely, ongoing and open communication between examiners and management or volunteers to enhance mutual understanding and to minimize surprises during the exam reporting process to the credit union’s board.”

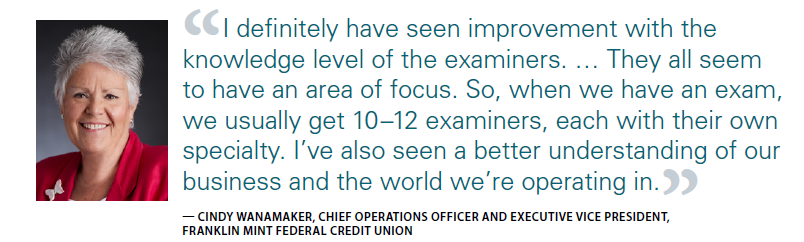

Wanamaker believes some of those efforts have paid off. “I definitely have seen improvement with the knowledge level of the examiners,” she says. “In the past, you’d get some who were a jack-of-all-trades, but that’s not the case anymore. Now, they all seem to have an area of focus. So, when we have an exam, we usually get 10–12 examiners, each with their own specialty. I’ve also seen a better understanding of our business and the world we’re operating in. Take cybersecurity. Even though it’s relatively new, we were impressed with examiners’ level of knowledge. They also took the time to listen to our IT folks and to make some good suggestions.”

Wanamaker’s experience is not universal, however. Bruyere notes that NAFCU still gets reports of examiner inconsistency and lack of knowledge. “We still hear that exams aren’t consistent across regions,” she says. “Recently, the Eastern Region asked credit unions to submit their board minutes. Board minutes had never been requested on an ongoing, monthly basis before. And, to our knowledge, no other region has made that request yet. We’re also hearing about inconsistency when it comes to examiners’ quality of knowledge regarding BSA.”

Another area of concern for Bruyere is the state of NCUA’s online resources intended to inform and support credit unions throughout the examination process. “Some documents in the examiner’s guide haven’t been updated in years,” she says. “Some documents are online-only, some are available as PDFs. We have seen some cases where NCUA has updated parts of their manual that aren’t publicly available.”

The NCUA in recent years began an exam modernization initiative, which is still being developed. The agency recommends subscribing to NCUA Express for real-time updates and important messages directly from the agency. Also, the agency says, “The Regulatory and Compliance Resources page of our NCUA.gov website is updated regularly and can provide useful information.”

A Compliance Culture

Bruyere acknowledges it’s true that “the exam process can effectively assess and encourage compliance,” but that compliance should not be considered something to be addressed only during exam preparation and follow-up. “A well-run credit union will … constantly [be] monitoring.” This is significant because, she notes, “there are plenty of laws organizations need to follow that may not come up in an examination.”

Because compliance should be a critical part of daily operations, Wanamaker believes it’s important for CEOs and others in leadership to share compliance information with staff regularly. Compliance must be kept front-of-mind if it’s to become an integral part of a credit union’s culture.

“Staff should know that we’re not taking all of these steps just for the heck of it and that compliance isn’t something only the big guys have to worry about,” she says. “How you handle compliance can impact the success of any credit union.”

John Fairbanks, public affairs specialist for NCUA, says the NCUA understands that, ultimately, every credit union is working toward success for its members and its community — and that’s what every NCUA exam is meant to assess. “NCUA’s goal during the examination process is to ensure every credit union is operated safely and soundly,” Fairbanks says. “This doesn’t mean credit unions can’t take risks. It does mean that we expect management to be aware of and to manage those risks.”

Robert Bittner is a Michigan-based freelance journalist and a frequent contributor to The NAFCU Journal.

This article was published in the November-December 2019 edition of The NAFCU Journal magazine. Want to receive The NAFCU Journal in your inbox? Update your email preferences.

Related Content

Related Content

- Compliance Blog: FFIEC Issues Policy Statement on Exam Reports

- Economic & CU Monitor: Special Report on NCUA Exams (member-only)

- The NAFCU Journal: Cybersecurity Exam Preparation

- Compliance Assistance: NAFCU’s Exam Fairness Guide